Spill Containment Systems Market Doubles on Regulatory Pressure and ESG Mandates (2026–2036)

The global spill containment systems market is entering a decade of accelerated expansion, driven less by optional safety upgrades and more by non-negotiable compliance, environmental accountability, and risk mitigation economics. As industries handling hazardous liquids face rising scrutiny from regulators, investors, and communities alike spill containment is shifting from a reactive safeguard to a core infrastructure requirement.

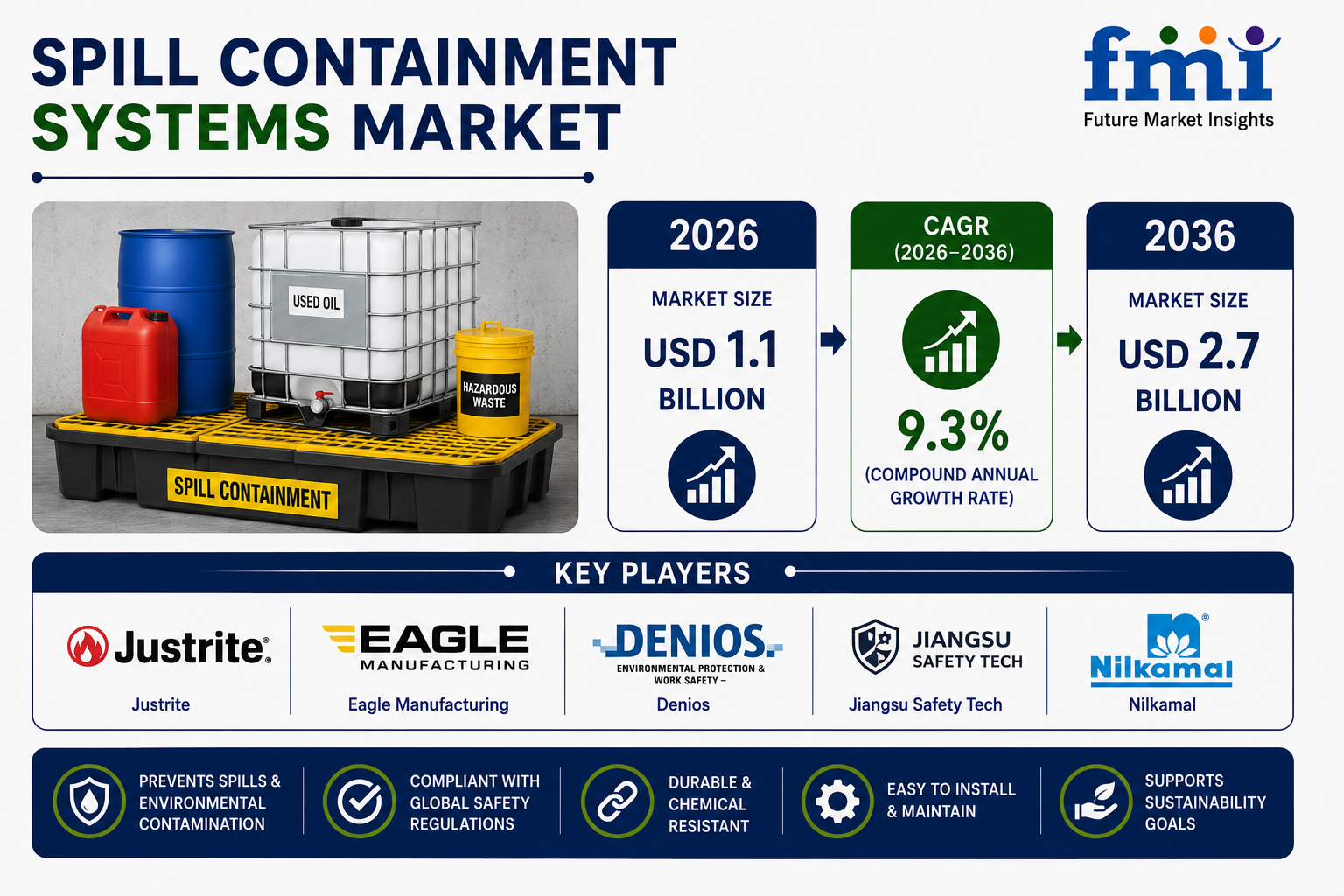

Quick Stats: Spill Containment Systems Market

- Market Size (2026): USD 1.1 billion

- Projected Value (2036): USD 2.7 billion

- CAGR (2026–2036): 9.3%

- Top End Use: Chemical & Oil Storage (40%)

- Leading Containment Type: Bunds, Berms & Pallets (45%)

- High-Growth Regions: India, China, USA, Brazil, Germany

Get Detailed Market Forecasts, Competitive Benchmarking, and Pricing Trends: https://www.futuremarketinsights.com/reports/sample/rep-gb-30289

Growth Drivers: Why Demand Is Accelerating

1. Regulatory Enforcement and Compliance Pressure

Governments worldwide are strengthening mandates around spill prevention and secondary containment. Facilities storing chemicals, fuels, and oils are now required to install engineered containment systems rather than relying on post-incident cleanup.

Non-compliance carries:

- Heavy fines

- Legal liabilities

- Operational shutdown risks

2. ESG and Corporate Accountability

Environmental, Social, and Governance (ESG) metrics are influencing capital allocation and procurement decisions. Spill containment systems directly support:

- Environmental protection goals

- Workplace safety standards

- Corporate sustainability reporting

Companies are increasingly investing in containment infrastructure to protect brand reputation and investor confidence.

3. Industrial Expansion in Emerging Markets

Rapid industrialization in countries like India and China is driving demand for spill containment systems across:

- Chemical manufacturing

- Oil & gas storage

- Warehousing and logistics

These regions are not only expanding capacity but also tightening environmental enforcement, accelerating adoption.

4. Rising Cost of Environmental Incidents

Spills today carry far greater financial consequences than before:

- Cleanup costs

- Regulatory penalties

- Production downtime

- Long-term environmental damage

This has shifted containment from a cost center to a risk management investment with measurable ROI.

Key Challenges: Barriers to Wider Adoption

- High Initial Investment: Advanced containment systems especially custom-engineered bunds and modular structures require significant upfront capital, which can slow adoption among SMEs.

- Infrastructure Constraints: Older facilities often lack the space or layout flexibility to install modern containment systems without redesign.

- Regulatory Fragmentation: Multinational operators must navigate different compliance standards across regions, complicating deployment strategies.

Opportunities: Where the Market Is Evolving

Smart Containment Systems

Integration of sensors and monitoring technologies is enabling:

- Early leak detection

- Real-time alerts

- Predictive maintenance

This transforms containment systems into active risk management tools.

Modular and Portable Solutions

Flexible containment systems are gaining traction, especially in:

- Temporary sites

- Remote operations

- Emergency response scenarios

These solutions reduce installation complexity and improve scalability.

Material Innovation

Advances in materials are improving:

- Chemical resistance

- Durability under extreme conditions

- Ease of maintenance

Manufacturers like Denios are focusing on engineered systems with enhanced performance and modular adaptability.

Segmentation Insights: Where Demand Is Concentrated

By End Use

- Chemical & Oil Storage (40%) dominates due to high spill risk

- Manufacturing and industrial safety sectors follow

- Warehousing & logistics are emerging as key adopters

By Containment Type

- Bunds, Berms & Pallets (45%) lead due to versatility and cost-effectiveness

- Spill decks and portable containment systems address specialized use cases

Companies such as Justrite and Eagle Manufacturing continue to dominate this segment with standardized and modular solutions.

Competitive Landscape: Engineering, Compliance, and Clarity

The competitive environment is defined by technical credibility and regulatory alignment, rather than branding alone.

Key Players:

- Justrite

- Eagle Manufacturing

- Denios

- TRUSCO Nakayama

- Nilkamal

Competitive Strategies:

- Modular system design for flexibility

- Clear technical documentation for compliance

- Focus on chemical resistance and durability

- Customization for industry-specific needs

The ability to simplify compliance for buyers is becoming a major differentiator.

Speak to Analyst: Customize insights for your Business Strategy: https://www.futuremarketinsights.com/customization-available/rep-gb-30289

Strategic Implications for Industry Stakeholders

- Spill containment is transitioning from reactive safety to proactive infrastructure

- Procurement teams must evaluate total risk reduction, not just upfront cost

- ESG compliance is becoming a primary purchasing driver

- Modular and scalable systems will dominate future deployments

- Integration with monitoring technologies will redefine value propositions

Future Outlook: The Next Phase of Market Evolution

1. Preventive Safety Becomes Standard: Containment systems will be embedded in facility design rather than retrofitted.

2. Smart Monitoring Integration: IoT-enabled containment will provide real-time risk visibility.

3. Regulatory Tightening Continues: Global standards will become stricter, driving consistent demand.

4. Expansion Across Emerging Markets: Industrial growth in Asia and Latin America will sustain long-term demand.

Executive Takeaways

- The spill containment systems market is set to more than double by 2036

- Growth is driven by regulation, ESG, and risk economics not optional upgrades

- Chemical & oil storage remains the dominant end-use segment

- India and China are the fastest-growing markets

- Technology integration and modular design are key competitive factors