Connected Vehicle Memory Industry Trends 2034

Memory Of Connected And Autonomous Vehicle Market Market Research Report

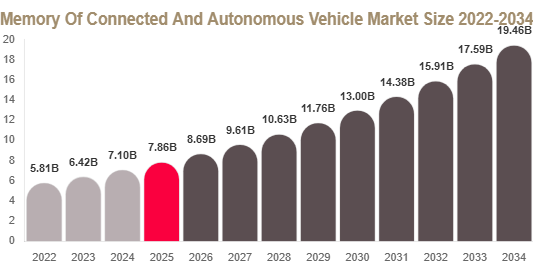

Market Size

The Memory Of Connected And Autonomous Vehicle Market Market size was valued at USD 6.48 Billion in 2025.

The market is projected to reach USD 18.92 Billion by 2034, growing at a CAGR of 12.67% during 2025–2034.

Get Your Sample Report Here:

https://www.redlinepulse.com/report/memory-of-connected-and-autonomous-vehicle-market/request-sample

Introduction

The memory of connected and autonomous vehicle market is emerging as a critical segment within the broader automotive electronics and intelligent mobility ecosystem. This market focuses on advanced memory solutions that support data processing, storage, and real-time decision-making in connected and self-driving vehicles. As autonomous driving systems become more sophisticated, the demand for high-speed, high-capacity, and low-latency memory technologies continues to increase rapidly across global automotive platforms.

Modern connected and autonomous vehicles generate massive volumes of data through sensors, cameras, radar systems, LiDAR, and onboard communication modules. This data must be processed in real time to ensure safe navigation, object detection, path planning, and vehicle-to-everything communication. Memory systems play a fundamental role in enabling these functions by ensuring seamless data flow between processors, control units, and AI-driven decision-making modules.

The increasing integration of artificial intelligence and machine learning in automotive systems has significantly elevated the importance of advanced memory architectures. Autonomous vehicles require memory solutions that can support high bandwidth, low power consumption, and extreme reliability under varying environmental conditions. As vehicles transition from assisted driving to fully autonomous operations, memory technologies are becoming central to system performance and safety.

The rapid evolution of connected mobility, smart transportation infrastructure, and vehicle electrification is further driving demand for automotive-grade memory solutions. Automakers and semiconductor manufacturers are investing heavily in next-generation memory technologies designed specifically for autonomous driving platforms. This transformation is expected to reshape the automotive electronics landscape over the forecast period.

Market Dynamics

Market Drivers

The increasing adoption of autonomous driving technologies is one of the primary drivers of the memory of connected and autonomous vehicle market. Self-driving vehicles rely heavily on continuous data processing from multiple sensors and AI systems, requiring high-performance memory solutions to ensure real-time responsiveness and decision accuracy. As autonomous vehicle testing and deployment expand globally, demand for advanced automotive memory systems continues to rise.

The rapid growth of connected vehicle ecosystems is also significantly contributing to market expansion. Vehicles today are equipped with advanced communication systems enabling connectivity with infrastructure, cloud platforms, and other vehicles. These systems generate continuous data streams that must be stored, processed, and transmitted efficiently, increasing reliance on high-speed memory architectures.

The increasing use of artificial intelligence in automotive systems further strengthens market growth. AI-driven applications such as predictive maintenance, autonomous navigation, driver monitoring, and advanced safety systems require substantial memory bandwidth and storage capacity. Memory technologies capable of supporting machine learning workloads are becoming essential components in modern vehicle architectures.

The expansion of electric vehicles and software-defined vehicles is additionally driving demand for advanced memory solutions. EVs rely on complex electronic control systems and centralized computing platforms that require efficient memory management for battery optimization, energy distribution, and autonomous functionality.

Market Challenges

Despite strong growth prospects, the market faces several technical and operational challenges. One of the primary concerns is the high cost associated with advanced automotive-grade memory solutions. High-performance memory components designed for autonomous vehicles require stringent testing, certification, and durability standards, increasing production costs significantly.

Thermal management and reliability under extreme automotive conditions also present major challenges. Memory systems used in vehicles must operate efficiently across wide temperature ranges while maintaining data integrity and system stability. Ensuring long-term reliability under continuous high-load conditions remains a key engineering challenge for manufacturers.

Cybersecurity risks associated with connected and autonomous vehicles also pose challenges to the market. As vehicles become increasingly connected, memory systems storing sensitive operational and user data become potential targets for cyber threats. Ensuring secure data storage and protection against unauthorized access is a critical industry requirement.

Another challenge involves supply chain constraints within the semiconductor industry. Automotive memory production depends on advanced semiconductor manufacturing processes, which are susceptible to global supply disruptions, raw material shortages, and geopolitical factors affecting production capacity.

Market Opportunities

The development of fully autonomous vehicles presents significant long-term opportunities for the memory of connected and autonomous vehicle market. Level 4 and Level 5 autonomous systems require highly advanced memory architectures capable of supporting real-time AI processing, sensor fusion, and complex decision-making algorithms.

The growing adoption of edge computing within vehicles also creates new opportunities. Edge computing reduces latency by processing data directly within the vehicle rather than relying solely on cloud systems. This increases demand for high-speed, localized memory systems optimized for onboard processing capabilities.

Expansion of smart transportation infrastructure, including intelligent traffic systems and connected mobility platforms, is expected to further boost demand for automotive memory solutions. Integration between vehicles and infrastructure will require continuous data exchange and real-time analytics, increasing memory requirements across automotive systems.

Technological advancements in next-generation memory types such as DRAM, NAND flash, and emerging non-volatile memory technologies are also opening new growth avenues. Manufacturers investing in high-density, low-power, and high-speed memory solutions are expected to gain strong competitive advantages.

Market Trends

One of the most significant trends in the market is the increasing adoption of high-bandwidth memory solutions in autonomous vehicle systems. These advanced memory architectures support faster data transfer rates, enabling real-time processing of sensor data required for safe autonomous navigation.

Another major trend is the shift toward centralized computing architectures in modern vehicles. Instead of distributed electronic control units, automakers are increasingly adopting centralized domain controllers that rely heavily on high-performance memory systems for efficient data processing and system integration.

The rise of software-defined vehicles is also shaping market development. These vehicles rely on continuous software updates and data-driven functionalities, requiring flexible and scalable memory architectures capable of supporting evolving automotive applications.

Additionally, automotive manufacturers are focusing on energy-efficient memory technologies to support electric vehicle performance. Low-power memory solutions help reduce overall energy consumption while maintaining high computational efficiency, aligning with sustainability goals and EV efficiency requirements.

Market Segmentation

The memory of connected and autonomous vehicle market is segmented based on memory type, application, vehicle type, level of autonomy, and storage architecture. By memory type, DRAM dominates due to its high-speed processing capabilities essential for real-time automotive applications. NAND flash memory also holds a significant share due to its role in data storage and infotainment systems.

Based on application, advanced driver assistance systems represent a major segment due to increasing integration of safety and automation technologies. Autonomous driving systems also account for significant demand as vehicles progress toward higher levels of autonomy requiring complex data processing capabilities.

In terms of vehicle type, passenger vehicles lead the market due to increasing consumer demand for connected and semi-autonomous features. Commercial vehicles are also experiencing growing adoption of advanced memory systems for fleet management, logistics optimization, and autonomous transport solutions.

By level of autonomy, Level 2 and Level 3 vehicles currently dominate due to widespread deployment of semi-autonomous driving technologies. However, Level 4 and Level 5 segments are expected to grow rapidly as fully autonomous vehicle testing and commercialization expand.

The market is further segmented by storage architecture into embedded memory systems and external storage solutions. Embedded memory systems dominate due to their integration within automotive electronic control units, while external storage solutions are gaining traction for data-intensive applications and cloud connectivity.

Regional Analysis

North America

North America holds a significant share of the memory of connected and autonomous vehicle market due to strong technological innovation and early adoption of autonomous driving systems. The United States leads regional demand with major investments in self-driving technologies and automotive AI development.

The region benefits from the presence of leading automotive technology companies, semiconductor manufacturers, and autonomous vehicle testing programs. Increasing collaboration between automotive OEMs and technology firms continues to drive innovation in automotive memory solutions.

Europe

Europe represents a major market driven by strong automotive manufacturing capabilities and advanced research in autonomous driving technologies. Countries such as Germany, France, and the United Kingdom are leading contributors to regional growth.

European automakers are heavily investing in connected vehicle platforms and intelligent mobility solutions. Strict regulatory standards for vehicle safety and emissions are also encouraging adoption of advanced memory technologies in automotive systems.

Asia Pacific

Asia Pacific is projected to witness the fastest growth in the market due to rapid expansion of automotive manufacturing and increasing investment in autonomous vehicle technologies. China, Japan, and South Korea are key contributors to regional development.

The region benefits from strong semiconductor manufacturing capabilities and rising demand for electric and connected vehicles. Government initiatives supporting smart transportation infrastructure are further accelerating market expansion.

Latin America

Latin America is experiencing gradual growth driven by increasing vehicle connectivity adoption and rising automotive technology integration. Brazil and Mexico are key markets contributing to regional development.

Improving transportation infrastructure and increasing awareness of automotive safety technologies are supporting demand for advanced memory solutions within connected vehicles.

Middle East & Africa

The Middle East & Africa region is witnessing steady growth due to increasing investments in smart city initiatives and advanced transportation systems. Gulf countries are leading adoption of connected mobility technologies.

Rising luxury vehicle adoption and growing interest in autonomous mobility solutions are expected to support long-term market development in the region.

Competitive Landscape

The memory of connected and autonomous vehicle market is highly competitive, driven by advancements in semiconductor technologies and automotive electronics innovation. Leading companies are focusing on developing high-speed, low-power, and highly reliable memory solutions tailored for autonomous driving applications.

Strategic collaborations between semiconductor manufacturers, automotive OEMs, and technology firms are shaping the competitive landscape. Companies are investing heavily in research and development to improve memory bandwidth, reduce latency, and enhance system reliability for autonomous vehicles.

Top Players Analysis

1. Samsung Electronics

Samsung Electronics is a key player in the automotive memory market, offering advanced DRAM and NAND flash solutions for connected and autonomous vehicles. The company focuses on high-performance memory technologies designed for AI-driven automotive systems.

Its strong semiconductor manufacturing capabilities and continuous innovation in memory architectures support its leadership position in the automotive electronics sector.

2. Micron Technology

Micron Technology plays a significant role in providing high-speed memory solutions for automotive applications. The company specializes in low-latency memory systems optimized for autonomous driving and connected vehicle platforms.

Its focus on reliability, energy efficiency, and automotive-grade certification strengthens its presence in the global market.

3. SK Hynix

SK Hynix is a leading semiconductor manufacturer offering advanced memory solutions tailored for automotive AI and autonomous systems. The company develops high-bandwidth memory products designed for real-time data processing in vehicles.

Its strong investment in next-generation memory technologies supports continued growth in the automotive electronics sector.

4. NXP Semiconductors

NXP Semiconductors focuses on integrated automotive solutions, including memory-related technologies for connected and autonomous vehicles. The company emphasizes secure and reliable data processing systems for automotive applications.

Its expertise in automotive electronics and system integration strengthens its competitive position.

5. Infineon Technologies

Infineon Technologies provides advanced semiconductor solutions supporting automotive memory and control systems. The company focuses on safety-critical applications and high-reliability automotive technologies.

Its strong presence in automotive electronics and power systems supports its long-term growth in the market.

Future Outlook

The future of the memory of connected and autonomous vehicle market is highly promising as autonomous driving technologies continue to evolve. Increasing demand for real-time data processing, AI integration, and high-speed communication systems will significantly drive memory innovation in the automotive sector.

Technological advancements in semiconductor design, edge computing, and high-bandwidth memory architectures will reshape automotive computing systems. Manufacturers will increasingly focus on developing scalable, energy-efficient, and ultra-reliable memory solutions for next-generation vehicles.

The expansion of fully autonomous vehicles and smart transportation ecosystems will further increase demand for advanced memory systems capable of supporting complex decision-making processes. Integration of AI, cloud connectivity, and vehicle-to-everything communication will continue driving market growth.

Emerging economies and global investments in smart mobility infrastructure will create substantial long-term opportunities. Companies capable of delivering high-performance, secure, and automotive-grade memory solutions will remain at the forefront of this rapidly evolving market.